What is the Sumbawa property market doing in 2026?

The Sumbawa property market in 2026 is in a pre-commercial window. The runway and terminal at Kiantar Airport are built and licensed. Commercial scheduled-flight status should be verified with a primary source dated within 60 days of any binding

decision. Land transactions on the Kertasari coastline have moved up since 2022 but remain a fraction of comparable Bali and Lombok parcels. The interesting question is what happens between now and the public flight schedule.

That gap is roughly eighteen months. It is the entire 2026 thesis. The Kiantar Airport pillar walks through the airport status in detail. This report covers the property-market layer.

Three things are simultaneously true. The infrastructure has arrived. Public commercial flights have not. Master-planned coastal supply has appeared where there was almost none in 2022. Whether the historical Indonesian airport-activation pattern repeats here is what every serious buyer is trying to size.

Where do Sumbawa land prices currently sit?

Sumbawa land prices currently span a wide band, structured by submarket, parcel quality, and the legal cleanliness of the title. Broker-reported listings give the cleanest snapshot, with the caveat that transaction-level data in Sumbawa remains thinner than in Lombok or Bali.

A representative comparable set, drawn from public broker listings and Indonesian property aggregators in early 2026:

| Property listing | Submarket | Plot size | Listing price | USD/m² | Source |

| Moyo Island absolute beachfront (FHL621) | Pulau Moyo | 23,248 m² | IDR 8.14 billion | ~USD 22 | Luxindo Property |

| Jelenga Bay panoramic hilltop (FHL615) | West Sumbawa (Scar Reef view) | 20,000 m² | USD 400,000 | USD 20 | Luxindo Property |

| Beachfront land Badas | Sumbawa (Badas) | 208,530 m² | IDR 15.5 billion | ~USD 4.7 | Rumah123 |

| Tourist land Pinisi Beach | West Sumbawa | 160,000 m² | IDR 20.8 billion | ~USD 8.1 | Rumah123 |

| Moyo Island coastal land bank | Pulau Moyo | 592,000 m² | IDR 11.8 billion | ~USD 1.3 | External market analysis report |

| Stunning beachfront land #364 | Sumbawa Besar (boat access) | 33,584 m² | USD 740,036 | USD 22 | Indonesia-Real.Estate |

| Tanah Phoenix Beach (Scar Reef) | Jelenga, Jereweh | 12,000 m² | IDR 14.4 billion | ~USD 75 | Rumah123 |

| Beachfront land Pulau Moyo (Labuan Aji) | Pulau Moyo | 2,758 m² | IDR 1.08 billion | ~USD 24 | Rumah123 |

| Roadside strategic land Alas Barat | Sumbawa (Alas Barat) | 1,000 m² | IDR 300 million | ~USD 19 | Rumah123 |

USD/m² calculated at IDR 16,000 = USD 1.

Three things to read out of this set. Per-m² prices for raw, undeveloped Sumbawa land cluster between USD 4 and USD 75 depending on submarket, parcel quality, road access, and beach exposure. Master-planned coastal estates command a meaningful premium over raw land, because they include infrastructure delivery, legal documentation, and registered title work. The Moyo Island land-bank entry is an outlier on the low end, reflecting raw remote-island parcels of unusual scale rather than a comparable for parcel-level pricing.

This is what a frontier coastal market looks like in its early years. Prices are wide. Comparables are uneven. The land-office registry is sparse compared with Lombok or Bali. Anyone quoting a single-number “Sumbawa price per square metre” is either oversimplifying or selling something.

How does Sumbawa compare to Bali and Lombok in 2026?

The price gap between West Sumbawa and Indonesia’s established resort markets is large and worth quantifying. Sumbawa coastal land currently transacts at single-digit and low-double-digit USD per square metre on raw parcels, and at USD 83-84 on master-planned estates. Bali Bukit and Canggu, the comparison the keyword targets, transact at multiples of that band. South Lombok sits in between.

Drawing from current external broker data:

| Market | Submarket | Prime beachfront / cliffside USD/m² (2025–2026 listings) | Source |

| Bali | Canggu / Berawa | USD 1,800–3,500+ | Seven Stones Indonesia, Investland Bali |

| Bali | Uluwatu / Pererenan | USD 1,800–3,500+ | Seven Stones Indonesia |

| Bali | Bukit cliffside (premium parcels) | USD 1,800–3,500+ | FazWaz |

| Bali | Sanur / Nusa Dua | USD 1,800–3,500+ | Seven Stones Indonesia |

| Lombok | Kuta / Tampah / Selong Belanak (well-located) | USD 200–600 | Nour Estates |

| Lombok | Mandalika beachfront (per-are listings) | USD 76–250 | South Lombok Land Sales |

| Lombok | Are Guling / Serangan / Torok (emerging) | USD 80–250 | Nour Estates |

| West Sumbawa | Master-planned coastal estate (Kertasari) | USD 83-84 | Rinjani Bay published pricing |

The headline number people focus on is the gap. A plot that would cost USD 500,000 in Canggu maps to roughly USD 30,000–50,000 for a comparable parcel in Kuta Lombok and roughly USD 5,000–10,000 in West Sumbawa raw-land terms. Nour Estates’ 2026 Bali vs Lombok comparison puts the Bali-to-Lombok price gap at 10×–50× depending on the specific submarket pairing. The Lombok-to-West-Sumbawa gap, on the data above, is similar in scale.

ROI is a more layered question than the price gap. Capital appreciation and rental yield move differently:

| Market | Typical villa rental yield (managed) | Capital-appreciation drivers |

| Bali Canggu / Uluwatu | 10–18% on well-managed villas (Nour Estates) | Saturation; supply growth keeping pace with demand; recent 12–18% annual price growth in prime areas (Prestige Property Bali) |

| Lombok South Coast | 15–18% ROI on total development cost; 30–50% land appreciation in key zones over 3 years (Nour Estates) | Mandalika SEZ build-out; MotoGP traffic; airport route expansion |

| West Sumbawa Kertasari | No mature managed-rental dataset yet | Pre-commercial: airport activation thesis; tourism scouting beginning |

The honest version is that Bali offers the deepest rental-yield infrastructure and the most established exit market. South Lombok offers stronger capital appreciation against a higher entry cost than Sumbawa. West Sumbawa offers the lowest entry cost and the highest single-event repricing potential, contingent on the Kiantar commercial activation playing out.

Where Sumbawa sits on a risk-adjusted basis depends on what the buyer is solving for. Yield seekers belong in Bali. Capital-growth-with-some-yield buyers belong in South Lombok. First-mover allocation belongs in West Sumbawa, sized appropriately for the time horizon and the pricing-uncertainty band.

Will Sumbawa land prices appreciate after Kiantar Airport opens?

Sumbawa land appreciation following Kiantar’s commercial activation is the central thesis question, and the honest answer in 2026 is not yet observable. The airport’s operating permit is in place. Charter flights are running. Scheduled commercial Bali service is anticipated mid-2027 but is not contracted. Industry-cited Indonesian precedent suggests that the largest land-price step-up follows commercial flight launch rather than infrastructure completion. The case rests on whether that pattern repeats. It is not a guarantee.

Two precedents anchor the discussion.

Lombok International Airport opened in 2011. Industry-cited broker commentary places beachfront and near-beach land-price increases in newly accessible South Lombok submarkets at 300–500% in the 36 months that followed. Wide variance by parcel. The Mandalika MotoGP circuit and the wave of branded-hotel investment that reshaped South Lombok dates from this airport activation.

Labuan Bajo’s Komodo Airport expanded in 2015. Land in the gateway town and along the harbour is commonly described as having tripled within 48 months. The market matured into one of Indonesia’s most active luxury-hospitality submarkets.

The destination state of an airport-driven activation curve is more useful as evidence than the appreciation figures alone. The Lombok airport in current numbers, fourteen years after activation:

| Lombok International Airport (BIZAM) | 2011 (opening) | 2025 (full year) |

| Annual passenger throughput | ~0 (newly opened) | 2.497 million |

| Annual aircraft movements | ~0 (newly opened) | 26,337 |

That is what an Indonesian regional gateway looks like once it has matured. Whether Kiantar travels the same curve depends on AMNT’s licensing posture, route economics, demand build, and the regional tourism environment. The wider environment is currently working in Kiantar’s favour. NTB province recorded 2.09 million tourism visits in the first ten months of 2025, with foreign arrivals in October up 25% year on year.

Two caveats worth carrying. The 300–500% Lombok figure is broker-reported, not peer-reviewed real-estate data. Treat it as directional. And “tripled” is an average over a wide spread. Some parcels did far more, some far less. Beachfront proximity, legal cleanness, and infrastructure are all decisive at the parcel level.

What’s the capital-growth case for Kertasari beach property in 2026?

The capital-growth case for Kertasari is precedent-anchored rather than forecast-anchored. There is no peer-reviewed appreciation forecast for the Kertasari coastline. There is industry-cited precedent (Lombok 2011, Labuan Bajo 2015), Rinjani Bay’s own internal projection band, and a set of conditions that determine whether Kertasari over- or underperforms the precedent. Treating any single forecast number as authoritative for a market of this thinness is a mistake the Patron buyer typically makes once.

What’s worth doing is bounding the case in scenarios.

- Underperformance scenario. Wings Air and TransNusa announce the route but the Bali frequency builds slowly. Initial loads come in at 30–40% in year one. International tourism remains Bali- and Lombok-focused. West Sumbawa land appreciation tracks Indonesian regional inflation plus a modest tourism premium. Outcome: 6–10% per year capital growth on Kertasari coastal land, in line with broader Indonesian property-market growth.

- Base-case scenario. Commercial Bali flights launch on the anticipated mid-2027 timeline. Wings Air and TransNusa operate daily by year-end 2027. Boutique hospitality announcements follow within 18 months. Foreign-direct-investment momentum in West Sumbawa gathers pace through 2028–2029. Outcome: appreciation tracking the lower end of the Indonesian-airport-activation precedent over a 5-year window. Translated into rough annualised terms, a 15–25% CAGR over the five-year period would land near the lower bound of the 300–500% Lombok pattern.

- Outperformance scenario. Kiantar gains international classification within five years. Major branded-hotel commitments appear (one-name brands, not just regional operators). Sumbawa benefits from Bali-overflow tourism the way South Lombok did from 2018 onward. Outcome: appreciation in the upper band of the Lombok 2011 precedent. The mid-30s annualised range sits within historical analogue.

- A self-citation disclosure. Rinjani Bay’s investment brochure projects 20–30% capital appreciation over five years for our own Kertasari plots, noted as “based on historical comparisons with similar Indonesian markets post-airport opening; past performance does not guarantee future results.” This is our internal projection. It is not an independently verified market forecast and we present it transparently rather than embedding it into the analysis. The base-case range above sits in roughly the same band but is anchored to the broader Lombok precedent rather than to internal modelling.

What kills any of these scenarios? Commercial flight launch slippage past 2028. AMNT scaling back its West Sumbawa industrial commitment. Indonesian regulatory drift on foreign-buyer leasehold structures. A material drop in Indonesian regional tourism demand. None of those are base-case expectations. All are real risks. The risks section addresses them directly.

Sumbawa submarkets: where the real money is moving

Five Sumbawa submarkets show meaningful 2026 transaction activity. They are not equivalent. Pricing, infrastructure, and buyer profile differ sharply across them, and parcels are not interchangeable.

- Kertasari coastline (West Sumbawa Regency). The cliffside corridor runs 20 minutes south of Kiantar Airport. Master-planned estate development concentrates here, Rinjani Bay being the largest single example at 46 hectares. Foreign-buyer-friendly leasehold structures predominate. Beachfront and cliff-top parcels with paved-road infrastructure sit at USD 83-84/m² on master-planned estates; raw-land equivalents in the corridor are scarce because most usable cliffside has already been consolidated. Tourism positioning emerges around manta-ray diving, surfing, and boutique eco-hospitality (Native Indonesia).

- Maluk and Sekongkang corridor. Down the west coast from Kertasari, traditionally a surfing community anchored by Super Suck and Yo-Yo’s. Pricing for hill-view and flat tourism land in Sekongkang sits in the USD 12–42/m² range on broker listings (Sumbawa Property). Infrastructure is improving but uneven. Buyer profile skews toward surfers and small-scale boutique operators rather than large estates.

- Jelenga and Scar Reef (Jereweh). The Phoenix Beach and Scar Reef parcels sit at the higher end of West Sumbawa raw-land pricing, with broker listings at USD 18–75/m² for tourism-zoned commercial parcels (Rumah123, Sumbawa Property). Surfing and tourism tailwind. Limited foreign-developed estate inventory at this point.

- Hu’u and Lakey Peak (central Sumbawa). The historic Sumbawa surf market, with seven world-class breaks (Lakey Peak, Periscopes, Nungas) within a small radius. Resort-scale beachfront parcels transact at USD 25–30/m² for raw land. The submarket sits ~6 hours by road from Kiantar Airport, which constrains its near-term appreciation against the Kertasari corridor.

- Pulau Moyo. Off the north coast, the island anchors Nihi Sumba’s sister property pipeline and the Amanwana legacy. Beachfront raw-land listings transact in the USD 20–25/m² range on residential-scale parcels and considerably lower on coastal land-bank scale (Indonesia-Real.Estate, Luxindo Property). Access is by boat. Buyer profile is ultra-private rather than commercial.

The Kiantar Airport activation thesis applies most cleanly to the Kertasari corridor, the Maluk/Sekongkang corridor, and to a more lagged extent Jelenga. Hu’u/Lakey and Pulau Moyo have their own access logistics that make them less directly geared to the Kiantar route map.

How can foreign buyers legally hold Sumbawa land?

Foreigners cannot hold the Hak Milik freehold title in Indonesia. The legal restriction is constitutional, applies across the country, and has not changed in any of the recent regulatory updates. The practical structures available to foreign buyers in Sumbawa are the same three available everywhere in the country, used in materially the same way they have been in Bali and Lombok for two decades.

- Hak Sewa (long-term leasehold). A registered lease agreement with a defined term, commonly 25, 50, or 90 years. The “90-year” headline figure typically describes a stacked extension structure rather than a single-instrument 90-year title. Industry-standard for villa and residential investments, including in master-planned estates. Registered with BPN (Badan Pertanahan Nasional). Fully transferable.

- Hak Pakai (right-of-use). Available to foreigners residing in Indonesia or to foreign companies with a local presence. Issued for up to 30 years, extendable to a longer total term by regulation. Most appropriate for personal residential property rather than commercial development.

- Rinjani Bay is offered as a 90-year leasehold (Hak Sewa).

What every honest version of this section should add: long-term leasehold is conditional, temporary, and subject to legal evolution. Engage independent Indonesian counsel before any commitment. Do not use nominee structures (an Indonesian citizen holding title on behalf of a foreigner) under any circumstances. Nominee arrangements are illegal, unenforceable, and carry well-documented risk of total capital loss. The major Indonesian property commentators are unanimous on this. So are we.

What are the actual risks?

The risks worth pricing in for West Sumbawa exposure in 2026 are not abstract.

- Commercial flight launch timing. Mid-2027 is anticipated, not contracted. Wings Air and TransNusa decisions depend on broader fleet and route-network economics. A realistic range is 12–24 months from this report.

- Single-operator dependence on the airport. Kiantar is owned by PT Amman Mineral Nusa Tenggara (AMNT). Phase 8 of the Batu Hijau mine commenced in May 2025, extending mine life to around 2030. The AMMAN smelter project adds further regional industrial commitment. AMNT is unlikely to wind down its West Sumbawa exposure on any near-term horizon. But the airport’s commercial-use posture remains a single operator’s decision in a way that would be unusual for an investment-grade gateway airport elsewhere.

- Indonesian leasehold structure. Headline term lengths describe stacked extension agreements rather than single-instrument titles. Engage independent counsel before any commitment. We will not pretend otherwise.

- Infrastructure beyond the airport. Roads, water, power, and telecommunications in Kertasari and the surrounding corridor are improving but uneven. On-estate infrastructure varies sharply between developments. The “completed-infrastructure” claim in any West Sumbawa marketing material deserves direct verification on site.

- Liquidity. West Sumbawa land is illiquid relative to Lombok and Bali. The buyer pool is smaller. Plan exit timelines in years, not months.

- Market-data sparseness. Honest engagement with West Sumbawa requires accepting that comparables are thinner than in mature markets. Most figures are agent-reported rather than registered with the land office. Treat any single-number “appreciation rate” with the scepticism warranted by frontier markets.

- Currency, taxation, and capital repatriation. Investments are typically USD-denominated; local costs are in IDR. Indonesian withholding tax applies to rental income (commonly 10–15%). Capital-gains tax applies on sale. Repatriation of funds is subject to Indonesian banking regulation. A tax adviser familiar with cross-border Indonesian property is essential.

- Natural disaster exposure. Indonesia is seismically active. Tropical weather events occur. Insurance coverage is widely available but does not eliminate event risk on a multi-decade time horizon.

- Regulatory drift. Indonesian foreign-property law has trended toward foreign-investor friendliness over the past five years (Omnibus Law, simplified PMA registration, longer leasehold extension regimes). Future drift in either direction is possible.

Where Rinjani Bay sits in this picture

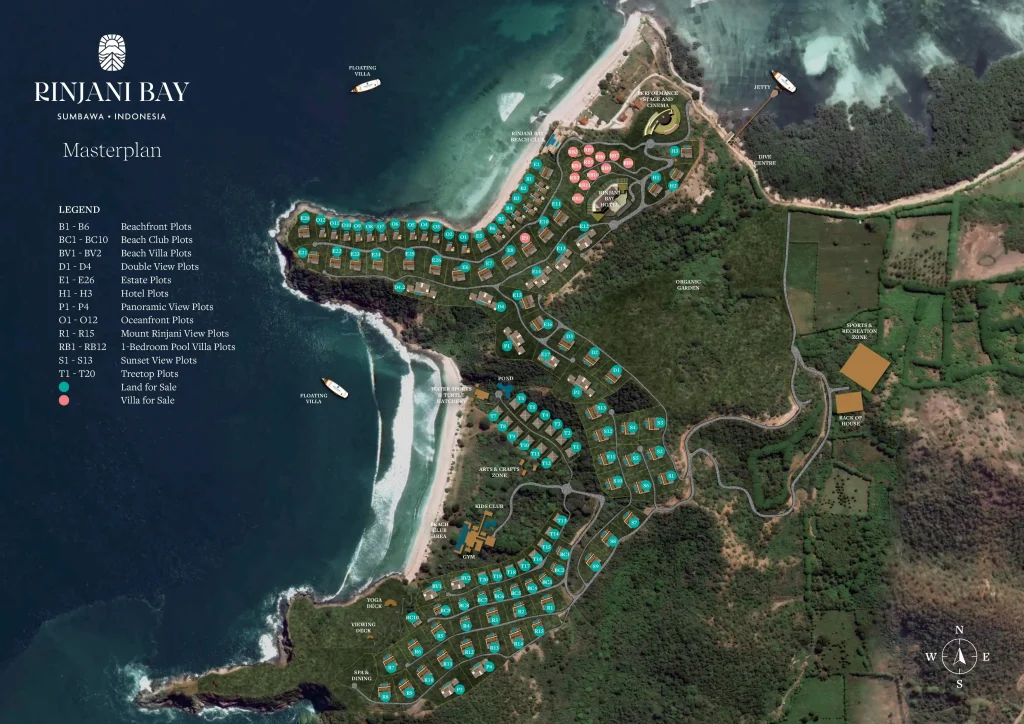

Rinjani Bay is a 46-hectare master-planned estate on the Kertasari cliffside, twenty minutes by road from Kiantar Airport. We are the publisher of this report. We have tried to keep the analysis honest about that.

Plot pricing currently runs USD 83-84 per square metre, depending on position, view exposure, and slope. The pricing band is inclusive of core infrastructure delivery (paved internal roads, stormwater systems, mainline electricity to plot boundary, municipal water), legal documentation, notary fees, and applicable land taxes. The 46 hectares inventory breaks down into:

- Beach Club Plots (BC series): USD 125,000 each, 921–1,469 m². Direct beachfront proximity to the Beach Club.

- Beach Villa Plots (BV series): USD 275,000 each, 2,000 m². Premium beachfront, largest plots in the estate.

- Panoramic View Plots (P series): USD 220,000–250,000, 2,657–4,892 m². Elevated headland with 270° ocean views.

- Double View Plots (D series): USD 175,000–220,000, 2,082–3,807 m². Ridge positions with ocean and valley views.

- More on The Opportunity

A separate turnkey 1-bedroom pool villa pathway is available for buyers who want a managed-yield position rather than land ownership, priced at USD 288,750 per villa with a contractual fixed annual lease fee.

Compared to the broader Sumbawa comparables in this report, Rinjani Bay sits at the master-planned-estate end of the pricing band. The premium over raw West Sumbawa land reflects infrastructure delivery, legal-structure work, the master-planning controls, and the operational backing of the broader Rascal Republic portfolio (Samara Lombok, Rascal Voyages).

For a serious buyer, the diligence questions worth a longer conversation are exact plot inventory, leasehold-structure mechanics, yield assumptions, comparable market data on the Kertasari corridor specifically, and exit assumptions. The Rinjani Bay estate brief walks through the detail. We strongly recommend independent legal, financial, and tax advice before any commitment. So does our own legal disclaimer.